Saving for your first home in Canada is a marathon, not a sprint. To help you cross the finish line faster, the federal government offers two major tax-advantaged tools: the First Home Savings Account (FHSA) and the Home Buyers’ Plan (HBP).

While they both aim to help you buy a home, they work very differently. Let’s break down which one you should prioritize to maximize your savings.

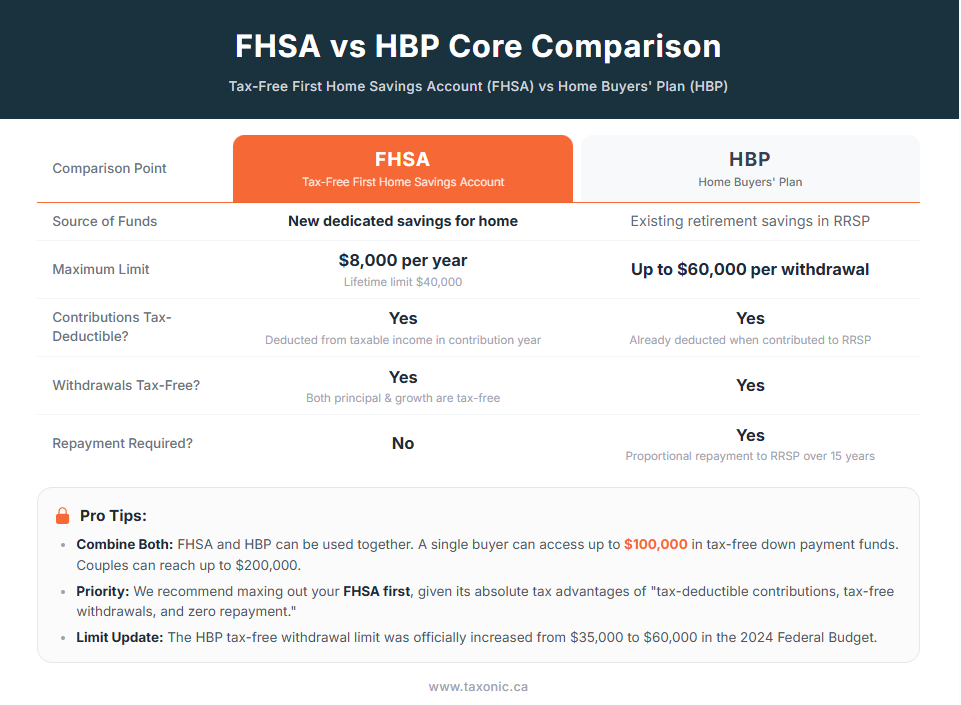

First Home Savings Account (FHSA)

The FHSA is a dedicated account for first-time buyers. It’s often called a hybrid because it combines the best features of an RRSP and a TFSA.

-

Tax-Deductible Contributions: Like an RRSP, every dollar you put in reduces your taxable income for the year, meaning a bigger tax refund.

-

Tax-Free Withdrawals: Like a TFSA, when you take the money out to buy your home (including any investment gains), you pay zero tax.

-

The Limits: You can contribute up to $8,000 per year, with a lifetime limit of $40,000.

-

The Best Part: Unlike the HBP, you never have to pay this money back. If you don’t buy a home within 15 years, you can roll the funds into your RRSP tax-free.

Home Buyers' Plan (HBP)

The HBP isn’t a separate account; it’s a rule that lets you “borrow” from your existing Registered Retirement Savings Plan (RRSP).

How it Works: Normally, pulling money out of an RRSP early triggers a massive tax bill. The HBP allows you to bypass that tax to fund your down payment.

The Limits: As of the 2024 Federal Budget, you can now withdraw up to $60,000 tax-free (up from the previous $35,000 limit).

The Catch (Repayment): This is a loan, not a gift. You must pay the money back into your RRSP over 15 years. If you miss a yearly repayment, that amount is added to your income for the year and taxed accordingly.

FHSA vs. HBP: At a Glance

Strategy: How to Maximize Your Benefits

The good news? You don’t have to choose. You can use both at the same time.

Between the two, a single buyer can access up to $100,000 ($40k from FHSA + $60k from HBP) in tax-advantaged funds. For a couple, that’s a massive $200,000 head start.

Recommended Order of Operations:

Max out your FHSA first: Because you don’t have to pay it back and the growth is tax-free, this is the most powerful tool in your shed.

Use the HBP as your “Top-Up”: If your FHSA isn’t enough to cover the down payment and you have funds sitting in your RRSP, tap into the HBP to bridge the gap.

We’re Here to Help

Smart tax planning can save you thousands during the home-buying process. Whether you’re trying to figure out your contribution room or need help navigating HBP repayments and tax filings, we’ve got your back.

Ready to make your move into the Canadian housing market? Contact us today for a personalized consultation.